Page loading...

Page loading...

-

Global Investment Performance Standards (GIPS®) for Fiduciary Management Providers to UK Pension Schemes

Download PDFExplanation of the Provisions in Sections 31-34

September 2020

GIPS® is a registered trademark owned by CFA Institute.

© 2020 CFA Institute. All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the copyright holder.

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is distributed with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional should be sought.

Introduction

The Global Investment Performance Standards (GIPS®) for Fiduciary Management Providers to UK Pension Schemes (GIPS standards for FMPs) are divided into four sections, which are as follows:

- Fundamentals of Compliance

- Input Data and Calculation Methodology

- Composite Maintenance

- GIPS Composite Report.

The Explanation of the Provisions in Sections 31-34 provides interpretation of each provision contained in Sections 31-34. Fiduciary Management Providers that choose to comply with the GIPS standards for FMPs must comply with all applicable requirements of the GIPS standards for FMPs, including any interpretative guidance published by CFA Institute and the GIPS standards for FMPs governing bodies.

Section 31: Fundamentals of Compliance.

The Fundamentals of Compliance section includes several core principles that create the foundation for the GIPS standards for FMPs, including properly defining the Fiduciary Management Provider, providing GIPS Composite Reports to all prospective clients, adhering to applicable laws and regulations, and ensuring that information presented is not false or misleading.Section 32: Input Data and Calculation Methodology.

Consistency of input data used to calculate performance is critical to effective compliance with the GIPS standards for FMPs and establishes the foundation for full, fair, and comparable investment performance presentations. Achieving comparability among Fiduciary Management Providers’ performance presentations requires uniformity in methods used to calculate returns. The GIPS standards for FMPs mandate the use of certain calculation methodologies to facilitate comparability. The Input Data and Calculation Methodology section addresses these topics.Section 33: Composite Maintenance.

A composite is an aggregation of one or more schemes managed according to a similar investment mandate, objective, or strategy. The composite return is the equal-weighted average of the performance of all scheme relative returns in the composite. Creating meaningful composites is essential to the fair presentation, consistency, and comparability of performance over time and among Fiduciary Management Providers.Section 34: GIPS Composite Report.

Section 34 includes the requirements and recommendations for preparing a GIPS Composite Report. Fiduciary Management Providers that prepare a GIPS Composite Report must include the required numerical information and disclosures specified in Section 34, if applicable to the specific composite.Each provision appears in a grey text box. Some words in the provisions are in small capital letters, which indicates defined terms that can be found in the GIPS Standards Glossary. Following each provision is a discussion that provides interpretive guidance to help readers understand the provision.

31. Fundamentals of Compliance

31.A. Fundamentals of Compliance - Requirements

Provision 31.A.1

The GIPS standards for Fiduciary Management Providers to UK Pension Schemes (GIPS standards for FMPs) MUST be applied on a FIDUCIARY MANAGEMENT PROVIDER-wide basis to those organizations that are subject to Part 6 of the Competition and Markets Authority Order. Compliance MUST be met on a FIDUCIARY MANAGEMENT PROVIDER-wide basis and cannot be met on a COMPOSITE or SCHEME basis.

Discussion

The GIPS standards for FMPs provide an ethical framework for calculating and presenting a Fiduciary Management Provider’s investment performance history. The definition of the Fiduciary Management Provider is the foundation for Fiduciary Management Provider-wide compliance and creates defined boundaries for determining the total Fiduciary Management Provider assets. Only Fiduciary Management Providers that are subject to Part 6 of the Competition and Markets Authority Order and manage actual assets for UK pension schemes may claim compliance with the GIPS standards for FMPs.

To claim compliance, a Fiduciary Management Provider must comply with all the applicable requirements of the GIPS standards for FMPs. Compliance cannot be met on a composite or scheme basis; it can be met only on a Fiduciary Management Provider-wide basis.

There is no requirement that the definition of the Fiduciary Management Provider, for the purpose of complying with the GIPS standards for FMPs, be the same as the legal entity. For example, if the legal entity also manages pension schemes outside of the United Kingdom, the Fiduciary Management Provider definition would include only UK pension schemes. There is no need for a separate legal entity to be created to accommodate this definition.

Provision 31.A.2

The FIDUCIARY MANAGEMENT PROVIDER MUST be defined to include all clients for which it acts as a FIDUCIARY MANAGEMENT PROVIDER.

Discussion

It is the Fiduciary Management Provider’s responsibility to ensure that the definition of the Fiduciary Management Provider is appropriate, rational, and fair. The definition of the Fiduciary Management Provider must include all UK pension schemes managed that are subject to Part 6 of the Competition Markets Authority Investigation Order (the Order). Equally important, the Fiduciary Management Provider definition must exclude any pension schemes that are not subject to the Order.

Generally, a Fiduciary Management Provider provides or offers the service of making investment decisions on behalf of the Pension Scheme Trustees on an ongoing basis, with respect to all or some of the pension scheme’s assets, for 100% of the full fiduciary management client assets. These actions are granted via written authority and discretion delegated by the Pension Scheme Trustees. There is no requirement that the definition of the Fiduciary Management Provider be the same as the legal entity.

Provision 31.A.3

To initially claim compliance with the GIPS standards for FMPs, the FIDUCIARY MANAGEMENT PROVIDER MUST attain compliance for a minimum of five years or for the period since the FIDUCIARY MANAGEMENT PROVIDER inception if the FIDUCIARY MANAGEMENT PROVIDER has been in existence for less than five years.

Discussion

A Fiduciary Management Provider cannot initially claim compliance with the GIPS standards for FMPs until it meets the applicable requirements of the GIPS standards for FMPs for at least a five-year period, or since inception if the Fiduciary Management Provider has been in existence for less than five years. Being in compliance for a minimum five-year period, or since inception if less than five years, means that for this period, the Fiduciary Management Provider has complied with all applicable requirements of the GIPS standards for FMPs, including any interpretive guidance published by CFA Institute and the GIPS standards governing bodies.

Assuming a Fiduciary Management Provider initially attains compliance for the minimum five-year period, it is required to present either five years of GIPS-compliant performance that complies with the GIPS standards for FMPs or performance since inception of the composite if it has been in existence less than five years. The ability to present five years of GIPS-compliant performance does not automatically mean, however, that the Fiduciary Management Provider can claim compliance with the GIPS standards for FMPs. The Fiduciary Management Provider must fulfill all of the requirements of the GIPS standards for FMPs for at least the initial five-year period or since inception if the Fiduciary Management Provider has been in existence for less than five years, not simply the requirements relating to the presentation of performance in a GIPS Composite Report. If a Fiduciary Management Provider initially claims compliance for a longer period than 5 years, the Fiduciary Management Provider must present a track record for the entire period for which it claims compliance, or for at least 10 years if the Fiduciary Management Provider claims compliance for a period longer than 10 years.

Once a Fiduciary Management Provider has claimed compliance for a 5-year period, or since inception of the Fiduciary Management Provider if the Fiduciary Management Provider has existed less than 5 years, the Fiduciary Management Provider must include in GIPS Composite Reports an additional year of performance each year, building up to a minimum of 10 years of compliant performance. Although a Fiduciary Management Provider is required to present only 10 years of performance in a GIPS Composite Report, it is recommended that Fiduciary Management Providers present more than 10 years of performance in a GIPS Composite Report.

Examples of time periods required to be presented when first claiming compliance with the GIPS standards for FMPs:

- Example 1:

A Fiduciary Management Provider has been in existence since 1 January 2011 and wishes to claim compliance starting with GIPS Composite Reports for periods ending 31 December 2019. The Fiduciary Management Provider decides to attain compliance for the minimum five-year period.

The Fiduciary Management Provider must comply with all applicable requirements of the GIPS standards for FMPs on a Fiduciary Management Provider-wide basis for an initial five-year period – in this case, from 1 January 2015 through 31 December 2019. The Fiduciary Management Provider must prepare GIPS Composite Reports that include five years of GIPS-compliant performance in its first GIPS Composite Reports for all composites that have a track record of at least five years. For all composites that have a track record of less than five years, the Fiduciary Management Provider must present a since-inception track record. The Fiduciary Management Provider must then continue to add one year of additional performance to its GIPS Composite Reports each year, building to a minimum of 10 years of GIPS-compliant performance for each composite – in this case, 1 January 2015 through 31 December 2024.

- Example 2:

A Fiduciary Management Provider has been in existence since 2003 and wishes to claim compliance starting in 2020. For various reasons, the Fiduciary Management Provider can create a GIPS-compliant track record only for the period 1 January 2017 through 31 December 2019.

The Fiduciary Management Provider may not claim compliance with the GIPS standards for FMPs until it can present five years of compliant performance. In this case, the Fiduciary Management Provider must wait two more years and add compliant returns for 2020 and 2021 before it can claim compliance with the GIPS standards for FMPs.

- Example 3:

A Fiduciary Management Provider has been in existence for two years and has two years of performance through 31 December 2019.

If a Fiduciary Management Provider has been in existence for less than five years, the Fiduciary Management Provider may claim compliance for the period since the Fiduciary Management Provider’s inception. The Fiduciary Management Provider must present performance since the composite inception date and then build to a minimum of 10 years of GIPS-compliant performance. In this case, the Fiduciary Management Provider may clam compliance with the GIPS standards for FMPs with 2 years of GIPS-compliant performance (2018 and 2019) and add an additional year each year until it reaches a minimum of 10 years of compliant performance. A Fiduciary Management Provider is not required to present a track record longer than 10 years but is recommended to do so.

- Example 4:

A Fiduciary Management Provider has been in existence for less than one year and has no annual composite performance to report.

The Fiduciary Management Provider may claim compliance with the GIPS standards for FMPs as soon as it meets all of the applicable requirements of the GIPS standards for FMPs and has performance to report. If the Fiduciary Management Provider is less than 12 months old, it is permitted to present since-inception performance in GIPS Composite Reports and claim compliance with the GIPS standards for FMPs.

Returns for periods of less than one year must not be annualized.

- Example 5:

A new Fiduciary Management Provider that does not yet manage UK pension scheme assets.

The Fiduciary Management Provider must notify prospective clients that it does not yet manage assets to one of the mandatory composite structures and therefore is not able to claim compliance with the GIPS standards for FMPs. The Fiduciary Management Provider may state that it has established policies and procedures to comply with the GIPS standards for FMPs once it has performance of assets managed for full fiduciary management clients (as specified by the Order) to report.

Provision 31.A.4

The FIDUCIARY MANAGEMENT PROVIDER MUST comply with all applicable REQUIREMENTS of the GIPS standards for FMPs, including any interpretive guidance published by CFA Institute and the GIPS standards for FMPs governing bodies.

Discussion

The GIPS standards for FMPs are ethical standards for investment performance presentation to ensure fair representation and full disclosure of a Fiduciary Management Provider’s performance. Fiduciary Management Providers must comply with all the requirements of the GIPS standards for FMPs that apply to the Fiduciary Management Provider, including requirements found within the provisions of the GIPS standards for FMPs as well as any guidance published by CFA Institute and the GIPS standards for FMPs governing bodies. Fiduciary Management Providers must also comply with all updates and clarifications published by these entities. This requirement is limited to guidance that relates specifically to GIPS standards for FMPs. Fiduciary Management Providers must review all of the provisions and other requirements of the GIPS standards for FMPs to determine each requirement’s applicability.

The GIPS standards for FMPs must be applied with the objectives of fair representation and full disclosure of investment performance. Meeting the objectives of fair representation and full disclosure will likely require compliance with more than the minimum requirements of the GIPS standards for FMPs. If a Fiduciary Management Provider applies the GIPS standards for FMPs in a performance situation that is not addressed specifically by the GIPS standards for FMPs or is open to interpretation, disclosures other than those required by the GIPS standards for FMPs may be necessary. To fully explain the performance included in a GIPS Composite Report, Fiduciary Management Providers are encouraged to present all relevant information, beyond required and recommended information, that will help a prospective client understand the information presented. Fiduciary Management Providers are also encouraged to adopt the recommendations included in the GIPS standards for FMPs.

Provision 31.A.5

The FIDUCIARY MANAGEMENT PROVIDER MUST:

- Document its policies and procedures used in establishing and maintaining compliance with the REQUIREMENTS of the GIPS standards for FMPs, as well as any RECOMMENDATIONS it has chosen to adopt, and apply them consistently.

- Create policies and procedures to monitor and identify changes and additions to the GIPS standards for FMPs, including any guidance published by CFA Institute and the GIPS standards for FMPs governing bodies.

Discussion

Policies and procedures are essential to implementing adequate business controls at all stages of the investment performance process – from data input to preparing marketing materials – to ensure the validity of the claim of compliance. A Fiduciary Management Provider must document all of the policies and procedures it follows for meeting the requirements of the GIPS standards for FMPs, as well as any recommendations the Fiduciary Management Provider has chosen to adopt. There is no requirement to create and document policies and procedures to comply with requirements that do not apply to the Fiduciary Management Provider. Fiduciary Management Providers must actively make a determination about the applicability of all the requirements of the GIPS standards for FMPs, however, and document their policies and procedures accordingly.

Once a Fiduciary Management Provider establishes its policies and procedures, it must apply them consistently. Policies and procedures should be reviewed regularly to determine if they should be changed or improved, but it is not expected that they will change frequently. A Fiduciary Management Provider must not change a policy retroactively solely to enhance performance or to present the Fiduciary Management Provider in a better light. Retroactive changes to policies and procedures should be avoided.

Fiduciary Management Providers must also create policies and procedures to monitor and identify changes and additions to the GIPS standards for FMPs as well as guidance published by CFA Institute and the GIPS standards for FMPs governing bodies. A Fiduciary Management Provider should assign at least one person internally who is responsible for monitoring its compliance with the GIPS standards for FMPs. Depending on the Fiduciary Management Provider’s size and complexity, it might have a team of people responsible for monitoring and maintaining compliance with the GIPS standards for FMPs. Maintaining compliance may require coordination across multiple departments, including but not limited to operations, performance, compliance, and marketing.

Provision 31.A.6

The FIDUCIARY MANAGEMENT PROVIDER MUST:

- Comply with all applicable laws and regulations regarding the calculation and presentation of performance.

- Create policies and procedures to monitor and identify changes and additions to laws and regulations regarding the calculation and presentation of performance.

Discussion

The GIPS standards for FMPs provide an ethical framework for calculating and presenting a Fiduciary Management Provider’s investment performance history. Fiduciary Management Providers must also comply with all applicable laws and regulations regarding the calculation and presentation of performance in the country or countries in which they are domiciled as well as those countries in which they do business. Fiduciary Management Providers must create policies and procedures to ensure that they adhere to all applicable laws and regulations regarding the calculation and presentation of performance. Fiduciary Management Providers must also have policies and procedures to identify and monitor changes and additions to laws and regulations regarding the calculation and presentation of performance.

Compliance with applicable laws and regulations does not necessarily result in compliance with the GIPS standards for FMPs. Fiduciary Management Providers claiming compliance must comply with the GIPS standards for FMPs in addition to all applicable laws and regulations. In the rare cases in which laws and regulations conflict with the GIPS standards for FMPs, Fiduciary Management Providers are required to comply with the laws and regulations and disclose the manner in which the laws and/or regulations conflict with the GIPS standards for FMPs.

Provision 31.A.7

The FIDUCIARY MANAGEMENT PROVIDER MUST not present performance or PERFORMANCE-RELATED INFORMATION that is false or misleading. This REQUIREMENT applies to all PERFORMANCE OR PERFORMANCE-RELATED INFORMATION on a FIDUCIARY MANAGEMENT PROVIDER-wide basis and is not limited to those materials that reference the GIPS standards for FMPs. The fiduciary management provider may provide any performance or PERFORMANCE-RELATED INFORMATION that is specifically requested by a prospective client for use in a one-on-one presentation.

Discussion

The underlying principles of the GIPS standards for FMPs, fair representation and full disclosure, help to ensure that current and prospective clients are not given performance or performance-related information that is incomplete, inaccurate, biased, or fraudulent. Fiduciary Management Providers must not present any performance or performance-related information that is known to be inaccurate or that may mislead either prospective or current clients. This concept applies to all performance or performance-related materials on a Fiduciary Management Providerwide basis and is not limited to those materials that reference the GIPS standards for FMPs.

Fiduciary Management Providers are not limited to providing only GIPS-compliant information to prospective clients or other interested parties. Fiduciary Management Providers may present other performance or performance-related information as long as it is not false or misleading.

The following information has an especially high risk of being interpreted by prospective clients in a way that is likely to be false or misleading:

- Actual performance linked to model, hypothetical, backtested, or simulated historical results; and

- Non-portable performance from a past Fiduciary Management Provider linked to current ongoing results.

This linked information must not be presented in a GIPS Composite Report.

Outside of a GIPS Composite Report, Fiduciary Management Providers may present this linked information if asked to do so by a prospective client. The linked information may be presented in a one-on-one presentation that is created for and will be used only by the prospective client.

The linked information may also be presented outside of a GIPS Report in marketing materials provided to other prospective clients if the following conditions are met:

- The linked information is presented in a one-on-one presentation that includes the delivery of a GIPS Composite Report, if the corresponding GIPS Composite Report has not been previously delivered to the prospective client;

- The linked information is presented only to prospective clients who the Fiduciary Management Provider believes are sufficiently knowledgeable about investments and can understand the relevance and limitations of the track record being presented;

- There are sufficient disclosures regarding the linked information so that prospective clients understand that it is not a GIPS-compliant track record. Disclosure, however, does not necessarily prevent information from being false or misleading;

- The linked information is not presented if a GIPS-compliant track record is requested; and

- The linked information is not included in a consultant database.

A Fiduciary Management Provider may wish to present performance for select time periods, other than the time period(s) required and recommended by the GIPS standards for FMPs. For example, if the market experienced a sharp decline during the first two months of the calendar year and became more stable in March, the Fiduciary Management Provider may want to show performance of its strategy from 1 January through 28 February and from 1 March through 31 December. If the performance for these select time periods is presented in addition to the performance for the required time periods, it may be presented in a GIPS Composite Report. This is permitted because the select time periods are being presented in addition to the required time periods. To present only performance for the select time periods without performance for the required time periods, especially if the select time periods were chosen because the periods had the highest performance, would be misleading and is not permitted for Fiduciary Management Providers that claim compliance with the GIPS standards for FMPs. Fiduciary Management Providers may present performance for select time periods outside of GIPS Composite Reports with the appropriate disclosure and labeling.

The Fiduciary Management Provider may provide to a prospective client any information requested by that prospective client. Such information must be restricted to a one-on-one presentation for use with that specific prospective client and must be accompanied by comprehensive disclosures that explain the information being presented. A one-on-one presentation is not limited to a formal presentation or to information presented in a face-to-face meeting. A one-on-one presentation refers to a presentation that is created for and will be used only by the prospective client who made the request.

Provision 31.A.8

If the FIDUCIARY MANAGEMENT PROVIDER does not meet all the applicable REQUIREMENTS of the GIPS standards for FMPs, the FIDUCIARY MANAGEMENT PROVIDER MUST NOT represent or state that it is “in compliance with the GIPS standards for FMPs except for…” or make any other statements that may indicate compliance or partial compliance with the GIPS standards for FMPs.

Discussion

When a Fiduciary Management Provider makes the claim of compliance with the GIPS standards for FMPs, it is representing that all of the applicable requirements of the GIPS standards for FMPs have been met on a Fiduciary Management Provider-wide basis. Either a Fiduciary Management Provider meets all of the applicable requirements of the GIPS standards for FMPs and may claim compliance, or a Fiduciary Management Provider does not meet all of the applicable requirements of the GIPS standards for FMPs and must not claim compliance or partial compliance with the GIPS standards for FMPs. If the Fiduciary Management Provider does not meet all of the applicable requirements of the GIPS standards for FMPs, the Fiduciary Management Provider must not represent or state that it is “in compliance with the GIPS standards for FMPs except for…” or make any other statements that may indicate compliance or partial compliance with the GIPS standards for FMPs.

Provision 31.A.9

Statements referring to the calculation methodology as being “in accordance,” “in compliance,” or “consistent” with the GIPS standards for FMPs, or similar statements, are prohibited.

Discussion

Only Fiduciary Management Providers that manage actual assets may claim compliance with the GIPS standards for FMPs.

For Fiduciary Management Providers that do manage actual assets, either directly or through the use of sub-advisors, compliance can be achieved only when the Fiduciary Management Provider has met all of the applicable requirements of the GIPS standards for FMPs on a Fiduciary Management Provider-wide basis. Compliance with the GIPS standards for FMPs involves more than simply using a particular calculation methodology. To avoid any confusion, references to the GIPS standards for FMPs must not be used in the context of reporting performance or performance presentations when the Fiduciary Management Provider is not in compliance with the GIPS standards for FMPs.

Software vendors, custodians, and other service providers do not manage actual assets and cannot claim compliance with the GIPS standards for FMPs. They may make reference to the fact that their software or services may help a Fiduciary Management Provider achieve or maintain compliance with the GIPS standards for FMPs, if that is the case. For example, a software vendor may state that its software system calculates performance that satisfies the calculation requirements of the GIPS standards for FMPs, but the vendor must not state or imply that using its system automatically makes a Fiduciary Management Provider compliant with the GIPS standards for FMPs or that its system complies with the GIPS standards for FMPs.

Consultant databases or questionnaires often require Fiduciary Management Providers to fill in monthly or quarterly performance data. The databases or questionnaires then ask the Fiduciary Management Provider to indicate whether or not the data presented has been prepared in accordance with the GIPS standards for FMPs. When responding to such a database or questionnaire, a Fiduciary Management Provider that claims compliance with the GIPS standards for FMPs may state that the returns “are prepared in compliance with the GIPS standards for FMPs” if the following conditions are met:

- The performance information used to complete the questionnaire is consistent with the information used to prepare the corresponding GIPS Composite Report;

- If applicable, the performance information used to complete the questionnaire is more current than the information currently included in the corresponding GIPS Composite Report but will be used in the future to update the corresponding GIPS Composite Report; and

- If applicable, the performance information used to complete the questionnaire is older than the information currently included in the corresponding GIPS Composite Report but could have been used to report the composite’s performance for periods prior to those currently included in the GIPS Composite Report.

Provision 31.A.10

The FIDUCIARY MANAGEMENT PROVIDER MUST NOT make statements referring to the performance of a current client as being “calculated in accordance with the GIPS standards for FMPs,” except for when a FIDUCIARY MANAGEMENT PROVIDER that claims compliance with the GIPS standards for FMPs reports the performance of a SCHEME to current clients.

Discussion

The GIPS standards for FMPs do not specifically address how a Fiduciary Management Provider must report performance of an individual client’s scheme to current clients. The GIPS standards for FMPs do provide an ethical framework for calculating and presenting a Fiduciary Management Provider’s investment performance history, allowing both prospective and current clients the best opportunity to fairly evaluate the Fiduciary Management Provider’s past performance.

The Fiduciary Management Provider must not make statements referring to a current client’s performance as being “calculated in accordance with the GIPS standards for FMPs,” except for when a GIPS-compliant Fiduciary Management Provider reports the performance of a scheme to current clients. When a Fiduciary Management Provider that claims compliance with the GIPS standards for FMPs reports the performance of a current client’s scheme to that client, the Fiduciary Management Provider may note on the current client’s performance report, if applicable, that the return was calculated in accordance with the requirements of the GIPS standards for FMPs.

Provision 31.A.11

The FIDUCIARY MANAGEMENT PROVIDER MUST make every reasonable effort to provide a GIPS COMPOSITE REPORT to all PROSPECTIVE CLIENTS when they initially become PROSPECTIVE CLIENTS. The FIDUCIARY MANAGEMENT PROVIDER MUST NOT choose to which PROSPECTIVE CLIENTS it presents a GIPS COMPOSITE REPORT.

Discussion

Fiduciary Management Providers claiming compliance with the GIPS standards for FMPs must make every reasonable effort to provide all prospective clients with a GIPS Composite Report when they initially become prospective clients. The GIPS Composite Report must be one that represents the strategy being marketed to the prospective client. The Fiduciary Management Provider must not choose to which prospective clients it presents a GIPS Composite Report.

A GIPS Composite Report is defined as a presentation for a composite that contains all the information required by the GIPS standards for FMPs and may include recommended information. It may also include other information that the Fiduciary Management Provider believes would be helpful to interpreting the GIPS Composite Report. A prospective client is defined as an entity that has expressed interest in one of the Fiduciary Management Provider’s composite strategies and qualifies to invest in the composite. Current clients may also qualify as prospective clients for any strategy that differs from their current investment strategy. Providing a GIPS Composite Report to current clients interested in a strategy different from their current strategy will help ensure that they have the information necessary to evaluate the new investment strategy and make an informed decision. Investment consultants, consultant databases, and other third parties are considered prospective clients if they represent entities that qualify as prospective clients.

It is up to the Fiduciary Management Provider to establish policies and procedures for determining who is considered to be a prospective client. These include policies and procedures for determining when an interested party becomes a prospective client. An interested party becomes a prospective client when two tests are met. First, the interested party must have expressed interest in a specific composite strategy or strategies. Second, the Fiduciary Management Provider must have determined that the interested party qualifies to invest in the respective composite strategy. For example, assume a Fiduciary Management Provider is meeting with an interested party to introduce the Fiduciary Management Provider to the interested party. At this initial meeting, the Fiduciary Management Provider provides information about itself in an attempt to interest the interested party in investing with the Fiduciary Management Provider. At this point, the two tests to qualify as a prospective client have not been met; therefore, the interested party is not yet a prospective client, and the Fiduciary Management Provider is not obligated to provide a GIPS Composite Report. The Fiduciary Management Provider should, however, communicate that it claims compliance with the GIPS standards for FMPs and offer to provide a list of all composite descriptions.

Once the interested party expresses interest in a specific composite strategy and the Fiduciary Management Provider determines that the interested party qualifies to invest in the composite strategy, the interested party then becomes a prospective client. This is the point at which the Fiduciary Management Provider must make every reasonable effort to provide the prospective client with the appropriate GIPS Composite Report, if the Fiduciary Management Provider has not already provided it to the prospective client.

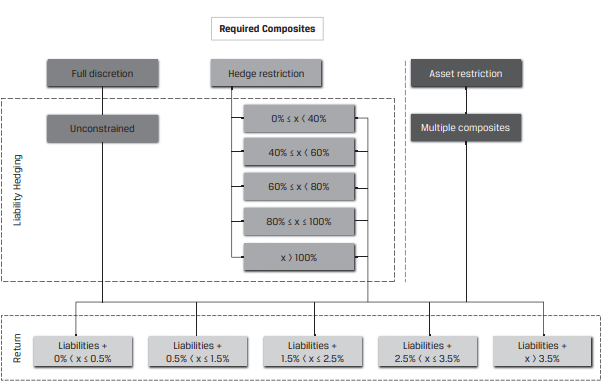

At times, a prospective client may ask the Fiduciary Management Provider about a composite strategy that the Fiduciary Management Provider does not yet manage. For example, assume a Fiduciary Management Provider manages schemes included in two composites. One is the Liabilities + 0% < x ≤ 0.5% unconstrained composite, and the other is the Liabilities + 0% < x ≤ 0.5% hedge restriction 40% ≤ x < 60% composite. The prospective client originally was interested in (and qualified to invest in) the unconstrained composite. The prospective client learns that the Fiduciary Management Provider also manages hedge-restricted strategies but does not currently have a Liabilities + 0% < x ≤ 0.5% hedge restriction 60% ≤ x < 80% composite that the prospect is looking for. If the Fiduciary Management Provider does not have an appropriate composite to present to the prospective client, the Fiduciary Management Provider must inform the prospective client that it does not currently manage the specific style or strategy.

Because a Fiduciary Management Provider is required to demonstrate that it made every reasonable effort to provide prospective clients with a GIPS Composite Report (see Provision 31.A.14), a Fiduciary Management Provider should establish policies and procedures for tracking which GIPS Composite Reports or initial partial-period performance outside of a GIPS Composite Report were provided to which prospective clients, and when. Doing so will allow a Fiduciary

Management Provider to determine when ongoing prospective clients must receive an updated GIPS Composite Report. (See Provision 31.A.12 regarding the requirement to provide an updated GIPS Composite Report to ongoing prospective clients.) It will also allow a Fiduciary Management Provider to know who must receive a corrected GIPS Composite Report in cases for which the Fiduciary Management Provider determines that a previously distributed GIPS Composite Report contained a material error. (See Provision 31.A.15.)

It is the Fiduciary Management Provider’s obligation to make every reasonable effort to provide a GIPS Composite Report to prospective clients. The Fiduciary Management Provider may do so by providing the GIPS Composite Report directly to the prospective client or by providing the prospective client with an electronic link to the GIPS Composite Report. The link provided must be a direct link to the GIPS Composite Report, however, and not simply a general link to Fiduciary Management Provider information, such as a link to the Fiduciary Management Provider’s website.

Fiduciary Management Providers are not limited to providing only GIPS Composite Reports to prospective clients or interested parties. Fiduciary Management Providers may present other performance or performance-related information, in addition to the GIPS Composite Report, as long as it is not false or misleading. Fiduciary Management Providers may also provide any performance or performance-related information that a prospective client requests in a one-on-one presentation. Such information must be restricted to a one-on-one presentation for use with that specific prospective client and must be accompanied by comprehensive disclosures that explain the information being presented. A one-on-one presentation is not limited to a formal presentation or to information presented in a face-to-face meeting. In this case, the one-on-one presentation refers to a presentation that is created for and will be used only by the prospective client who made the request.

When a current client instructs a Fiduciary Management Provider to de-risk a scheme that is already managed by the Fiduciary Management Provider and does not first ask the Fiduciary Management Provider for information on the composite the scheme will move to, then the current client is not considered a prospect because the client is not “interested” in a new strategy. Instead, the client has already selected a new strategy. This scenario would qualify as a scheme that is changing strategy. (See the discussion of Provision 33.A.8 for documentation requirements for schemes that change investment mandates.)

Provision 31.A.12

Once the FIDUCIARY MANAGEMENT PROVIDER has provided a GIPS COMPOSITE REPORT to a PROSPECTIVE CLIENT, the FIDUCIARY MANAGEMENT PROVIDER MUST provide an updated GIPS COMPOSITE REPORT at least once every 12 months if the prospective client is still a prospective client.

Discussion

Some prospective clients remain prospective clients for extended periods of time. Once a Fiduciary Management Provider has provided a GIPS Composite Report to a prospective client, the Fiduciary Management Provider must provide an updated GIPS Composite Report at least once every 12 months if the prospective client is still a prospective client. If a Fiduciary Management Provider provides performance information to an investment consultant or a database, these entities qualify as prospective clients and must receive the appropriate GIPS Composite Report(s). They must also receive an updated GIPS Composite Report at least once every 12 months.

Provision 31.A.13

When providing a GIPS COMPOSITE REPORT to PROSPECTIVE CLIENTS, the FIDUCIARY MANAGEMENT PROVIDER MUST update these reports to include information through the most recent annual period end within 12 months of that annual period end.

Discussion

GIPS Composite Reports have been designed to provide information to prospective clients that will help them understand the investment mandate, characteristics, and performance of a specific composite managed by the Fiduciary Management Provider. Although a GIPS Composite Report contains important information, the value and relevance of that information are affected by the timeliness with which the GIPS Composite Report is updated. A GIPS Composite Report containing returns that are significantly out of date is not helpful to prospective clients. It is therefore required that any GIPS Composite Report provided to a prospective client must be updated within 12 months of the most recent annual period end. As an example, GIPS Composite Reports for a composite with information through 31 December 2019 must be available no later than 31 December 2020, which would be within 12 months of the most recent calendar year end.

If a specific composite is not being marketed, and there are no prospective clients for the composite, the Fiduciary Management Provider is not required to update the GIPS Composite Report. As stated in Provision 31.A.18, however, a Fiduciary Management Provider must provide a GIPS Composite Report for any composite that is on the Fiduciary Management Provider’s list of composite descriptions to a prospective client upon request. Although a Fiduciary Management Provider is not required to annually update a GIPS Composite Report when there are no prospective clients for a composite, the Fiduciary Management Provider must be able to provide an updated GIPS Composite Report, within a reasonable period of time, to a prospective client for a composite.

Provision 31.A.14

The FIDUCIARY MANAGEMENT PROVIDER MUST be able to demonstrate how it made every reasonable effort to provide a GIPS COMPOSITE REPORT to those PROSPECTIVE CLIENTS REQUIRED to receive a GIPS COMPOSITE REPORT.

Discussion

Fiduciary Management Providers are required to make every reasonable effort to provide a GIPS Composite Report to all prospective clients. Fiduciary Management Providers are also required to have policies and procedures in place that are used to establish and maintain compliance with the requirements of the GIPS standards for FMPs. Therefore, any Fiduciary Management Provider claiming compliance with the GIPS standards for FMPs must have specific policies and procedures to ensure that every reasonable effort is made to provide the required GIPS Composite Report to prospective clients. These should include policies and procedures for tracking which GIPS Composite Reports were provided to which prospective clients, and when. For example, a Fiduciary Management Provider’s policies and procedures might specify that the required GIPS Composite Report will be included as part of the standard package of marketing materials prepared for prospective clients, and that a checklist will be used to indicate the dates on which the GIPS Composite Report was provided to the prospective client and which version of the GIPS Composite Report was provided. Documenting the date on which the GIPS Composite Report was last provided to the prospective client, as well as the version of the GIPS Composite Report, will help a Fiduciary Management Provider fulfill the requirement that the appropriate GIPS Composite Report be provided to a prospective client who remains a prospect at least once every 12 months. The most effective policies and procedures for a Fiduciary Management Provider will depend on the circumstances surrounding the typical interactions between the Fiduciary Management Provider and its prospective clients.

To demonstrate that the Fiduciary Management Provider made a reasonable effort to provide the appropriate GIPS Composite Report to prospective clients, it is necessary for the Fiduciary Management Provider to document both the relevant policies and procedures for providing the required reports to prospective clients and the steps taken to implement the relevant policies and procedures.

Provision 31.A.15

The FIDUCIARY MANAGEMENT PROVIDER MUST correct MATERIAL ERRORS in GIPS COMPOSITE REPORTS and MUST:

- Provide the corrected GIPS COMPOSITE REPORT to current clients that received the GIPS COMPOSITE REPORT that had the MATERIAL ERROR.

- Make every reasonable effort to provide the corrected GIPS COMPOSITE REPORT to all current PROSPECTIVE CLIENTS that received the GIPS COMPOSITE REPORT that had the MATERIAL ERROR. The FIDUCIARY MANAGEMENT PROVIDER is not REQUIRED to provide the corrected GIPS COMPOSITE REPORT to former clients or former PROSPECTIVE CLIENTS.

Discussion

Fiduciary Management Providers claiming compliance with the GIPS standards for FMPs are likely to face situations in which errors are discovered that must be specifically addressed. Even with the tightest of controls, errors will occur. An error, which can be qualitative or quantitative, is any component of a GIPS Composite Report that is missing or inaccurate. Errors in GIPS Composite Reports can result from, but are not limited to, incorrect, incomplete, or missing:

- composite relative returns or assets,

- total Fiduciary Management Provider assets,

- internal dispersion,

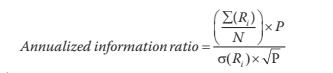

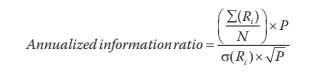

- information ratio,

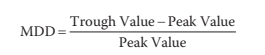

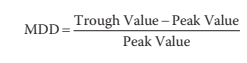

- maximum drawdown,

- number of schemes in a composite,

- three-year annualized ex post standard deviation, and

- disclosures.

Fiduciary Management Providers must establish error correction policies and procedures, and materiality must be defined in the error correction policies.

If a GIPS Composite Report contains a material error, the GIPS Composite Report must be corrected and the corrected GIPS Composite Report that includes a disclosure of the error must be provided to all current clients who received the GIPS Composite Report with the material error. The Fiduciary Management Provider must also make every reasonable effort to provide the corrected GIPS Composite Report to all current prospective clients that received the GIPS Composite Report with the material error. The Fiduciary Management Provider is not required to provide the corrected GIPS Composite Report to former clients and former prospective clients that received the GIPS Composite Report that contained the material error.

The Fiduciary Management Provider generally has three options for dealing with non-material errors in GIPS Composite Reports:

- Take no action.

The error is deemed immaterial and does not require a change to any data or disclosures in the GIPS Composite Report. - Correct the GIPS Composite Report with no disclosure of the change and no distribution of the corrected GIPS Composite Report.

The correction of the error results in a change to one or more items in the GIPS Composite Report, but these changes are deemed not material and therefore do not require disclosure of the change or distribution of the corrected GIPS Composite Report. - Correct the GIPS Report with disclosure of the change and no distribution of the corrected GIPS Composite Report.

The correction of the error results in a change to one or more items in the GIPS Composite Report, but these changes are not deemed to be material. The Fiduciary Management Provider does not distribute the corrected GIPS Composite Report but, according to the Fiduciary Management Provider’s pre-established error correction policies and procedures, the error does require disclosure in the corrected GIPS Composite Report.

A Fiduciary Management Provider must decide what criteria it will use to determine materiality. The following is a definition of materiality that Fiduciary Management Providers might find useful as a starting point:

“An error (or item) is material if the magnitude of the omission or misstatement of performance presentation information, in light of surrounding circumstances, makes it probable that the judgement of a reasonable person relying on the information would have been changed by the omission or misstatement.”

When determining materiality, a Fiduciary Management Provider may consider the following factors:

- magnitude of the error, in absolute and relative terms,

- whether relative returns are overstated or understated,

- significance of the missing or incorrect disclosures,

- whether the error affects returns over time or is a timing issue,

- period(s) affected by the error,

- if these policies will be applied on a Fiduciary Management Provider-wide or a composite-specific basis, and

- whether the Fiduciary Management Provider has any legal or regulatory obligations related to error correction.

The size and effect of the error may vary for different types of information (e.g., composite relative returns versus risk measures), reporting periods (e.g., monthly, quarterly, or annual returns), and time periods (e.g., prior to a specific date or more than five years ago).

It is important to remember that the omission of required information is considered an error, as well as a misstatement in the information presented. The GIPS Composite Report must be corrected to include the required information, and the Fiduciary Management Provider must apply its error correction policies to determine if the error is material.

Fiduciary Management Providers must establish and document error correction policies and procedures and implement them consistently. A Fiduciary Management Provider should strive to create an unambiguous process that includes specific steps to discover and correct errors.

Provision 31.A.16

The FIDUCIARY MANAGEMENT PROVIDER MUST maintain a complete list of COMPOSITE DESCRIPTIONS. The FIDUCIARY MANAGEMENT PROVIDER MUST include terminated COMPOSITES on this list for at least five years after the COMPOSITE TERMINATION DATE.

Discussion

Fiduciary Management Providers must maintain a complete list of composite descriptions. Fiduciary Management Providers must include terminated composites on the Fiduciary Management Provider’s list of composite descriptions for at least five years after the composite termination date. One reason for this requirement is that a terminated composite may be restarted so a list of current and terminated composites may provide a more complete picture of a Fiduciary Management Provider’s capabilities.

A composite description provides key information about the investment strategy. The description is not meant to replace more-comprehensive descriptions of the investment strategy included in the composite definition or investment management agreement, but it should provide enough information about the strategy to be informative while remaining concise. It must provide enough information to prospective clients to make them aware of any significant features of a composite investment strategy that may distinguish the strategy from similar strategies within and between Fiduciary Management Providers. Composite descriptions must include information about the use of leverage, derivatives, and short positions, if they are a material part of the strategy, as well as if illiquid investments are a material part of the strategy.

When included on the list of composite descriptions, the composite description must also include the following information for each composite:

- composite name,

- composite creation date,

- composite inception date,

- composite termination date, if applicable, and

- number of schemes as of the most recent calendar year end.

Provision 31.A.17

The FIDUCIARY MANAGEMENT PROVIDER MUST provide the complete list of COMPOSITE DESCRIPTIONS to any PROSPECTIVE CLIENT that makes such a request.

Discussion

In addition to maintaining a complete list of composite descriptions, Fiduciary Management Providers must provide the list to any prospective client upon request. The discussion of Provision 31.A.16 addresses the creation of this list.

This list must include all of the Fiduciary Management Provider’s composites, including those that have terminated within the past five years. Although Fiduciary Management Providers are required to provide a complete list of composite descriptions to any prospective client that makes such a request, they are encouraged to provide this information to anyone else who makes the request.

Provision 31.A.18

The FIDUCIARY MANAGEMENT PROVIDER MUST provide a GIPS COMPOSITE REPORT for any COMPOSITE listed on the FIDUCIARY MANAGEMENT PROVIDER’S list of COMPOSITE DESCRIPTIONS to any PROSPECTIVE CLIENT that makes such a request.

Discussion

Provision 31.A.11 requires Fiduciary Management Providers to make every reasonable effort to provide the appropriate GIPS Composite Report to all prospective clients who are interested in a particular composite strategy. This provision requires a Fiduciary Management Provider to provide a GIPS Composite Report for any composite listed on the Fiduciary Management Provider’s list of composite descriptions to a prospective client upon request.

The Fiduciary Management Provider must therefore have the ability to prepare and provide a GIPS Composite Report for any composite on the Fiduciary Management Provider’s list of composite descriptions, including composites that are not typically marketed or that have been terminated within the past five years.

This requirement is an acknowledgement that, before investing with a Fiduciary Management Provider, a prospective client will often want to gain knowledge of the Fiduciary Management Provider that goes beyond information about the particular composite strategy in which they may want to invest. Requesting a GIPS Composite Report for other composites may help the prospective client gain a fuller picture of the investment activities of the Fiduciary Management Provider’s investment activities and a deeper understanding of the Fiduciary Management Provider with which they are considering investing.

Provision 31.A.19

All data and information necessary to support all items included in GIPS COMPOSITE REPORTS MUST be captured, maintained, and available within a reasonable time frame, for all periods presented in these reports.

Discussion

A fundamental principle of the GIPS standards for FMPs is the need for Fiduciary Management Providers to be able to ensure the validity of their claim of compliance. It is, therefore, important for current and prospective clients and regulators to have confidence that all items included in a GIPS Composite Report are supported by the appropriate records. This provision applies to GIPS Composite Reports for all composites, whether the composite is marketed or not.

Fiduciary Management Providers must maintain records to be able to recalculate their performance history as well as substantiate all other information included in a GIPS Composite Report for all periods shown. This requirement applies to all periods for which performance is presented in the GIPS Composite Report. If the regulators require records to be kept for longer periods than those required by the GIPS standards for FMPs, care should be taken to ensure that the Fiduciary Management Provider follows the strictest of the recordkeeping requirements applicable to the Fiduciary Management Provider.

It is understood that the required data may not be immediately available. For example, data may need to be retrieved from an offsite location or from a third-party service provider. However, the data and information required to be maintained by this provision must be available in a usable format within a reasonable time frame. In all instances, either paper (hard-copy) records or electronically stored records will suffice. If records are stored electronically, the records must be accessible and able to be printed or downloaded, if needed. Records stored in a system that is not operable and from which data cannot be retrieved will not satisfy the recordkeeping requirements.

Although most Fiduciary Management Providers are looking for a very precise list of the minimum documents that must be maintained to support all parts of the GIPS Composite Report, including the ability to recalculate the Fiduciary Management Provider’s performance history, there is no single list of records that will suffice in all situations. Each Fiduciary Management Provider must determine for itself which records must be maintained. The following lists include records that Fiduciary Management Providers should consider maintaining to meet the recordkeeping requirements of this provision. None of these lists should be considered exhaustive. The actual records required will depend on the Fiduciary Management Provider’s particular circumstances.

Records to Support Scheme-Level Returns

- scheme holdings reports, with investment positions and valuations, including information supporting the determination of fair value,

- information to prove that performance is based on actual assets, including bank/custodial statements and reconciliations,

- scheme transactions reports,

- outstanding trades reports,

- corporate action reports,

- income received/earned reports,

- accrued income reports,

- foreign or other withholding tax reclaim reports,

- cash flow/weighted cash flow reports,

- foreign exchange rates,

- support for scheme benchmark returns,

- information on calculation methodology used for scheme net returns and scheme relative returns,

- information provided by a third party (e.g., a sub-advisor or custodian) where it may be necessary for a Fiduciary Management Provider to take additional steps to ensure the information provided by the third party can be relied on to meet the requirements of the GIPS standards for FMPs, and

- investment management fee information.

Records to Support Composite-Level Returns and Other Composite-Level Data

- schemes included in the composite,

- when each scheme entered (and exited, if applicable) the composite,

- each scheme’s relative return for each period, and

- each scheme’s ending market value for each period,

- number of schemes in the composite and the composite assets as of each calendar year end, and any other period for which this information is presented in GIPS Composite Reports,

- internal dispersion calculation data,

- support for information ratio calculations,

- support for drawdown calculations, and

- support for annualized ex post standard deviation calculations.

Records to Support the Inclusion of a Scheme in a Specific Composite or Its Exclusion from All Composites

- composite definitions, particularly related to the composite inclusion criteria, including the definition of discretion,

- list of schemes excluded from composites, if any, and the reasons for exclusion,

- investment management agreements and investment guidelines and amendments thereto,

- reports provided to clients if used to help determine composite assignment,

- analytics used to support composite assignment or composite exclusion, and

- e-mail/other correspondence with clients regarding documented changes to a scheme’s investment mandate, objective, or strategy.

Records to Support a Fiduciary Management Provider’s Claim of Compliance

- GIPS standards for FMPs policies and procedures, covering all periods for which the Fiduciary Management Provider claims compliance with the GIPS standards for FMPs,

- definition of the Fiduciary Management Provider, historically and current,

- supporting calculation for total Fiduciary Management Provider assets reported as of each calendar year end and any other period for which total Fiduciary Management Provider assets is presented in GIPS Composite Reports,

- composite definitions, inception dates, and composite creation dates,

- list of composite descriptions,

- list of composite risks, and

- GIPS Composite Reports and supporting information for all composites.

Any Additional Records Necessary to Support a Claim of Compliance

- system and control reports from independent accountants or other third parties (e.g., accounting reports, other internal controls/compliance reports for the client and/or custodians),

- third-party (e.g., sub-advisory, custodial, performance data provider) agreements,

- minutes of relevant decision-making committees (e.g., a board, an investment committee, a GIPS compliance committee),

- systems manuals, especially for the systems that generate the scheme returns, composite returns, and GIPS Composite Reports,

- documentation of efforts made to provide all prospective clients with GIPS Composite Reports,

- documentation of efforts made to provide, in the case of a material error, a corrected GIPS Composite Report to all appropriate parties,

- underlying benchmark data (if not publicly available), and

- documentation of providing the following to any prospective client that made such a request:

- a GIPS Composite Report,

- a list of composite descriptions,

- a list of composite risks,

- policies for valuing schemes,

- policies for calculating performance, and

- policies for preparing GIPS Composite Reports.

It is expected that all Fiduciary Management Providers will have disaster recovery plans to mitigate the loss of records for any reason, whether from a catastrophic event beyond the control of the Fiduciary Management Provider or a situation within the control of the Fiduciary Management Provider. If a Fiduciary Management Provider that claims compliance with the GIPS standards for FMPs experiences a catastrophic event that destroys all of its records and electronic or other backup systems, the Fiduciary Management Provider should try to reconstruct the necessary information by obtaining the information from clients, custodians, consultants, or any other party outside the Fiduciary Management Provider that might have duplicate copies of those records. If the underlying data to support the GIPS Composite Report was destroyed because of extreme circumstances beyond the Fiduciary Management Provider’s control and is unavailable from other sources, however, the Fiduciary Management Provider may continue to claim compliance and show performance if the lack of records for the unavailable period(s) is disclosed.

For example, assume Fiduciary Management Provider A claims compliance with the GIPS standards for FMPs, and the records for Fiduciary Management Provider A from its inception on 1 January 2017 through 31 December 2017 were destroyed under extreme circumstances beyond the Fiduciary Management Provider’s control. The Fiduciary Management Provider can claim compliance with the GIPS standards for FMPs but must disclose that the Fiduciary Management Provider’s records for the period from 1 January 2017 through 31 December 2017 were destroyed under extreme circumstances beyond the Fiduciary Management Provider’s control and the data are unavailable from other sources. The Fiduciary Management Provider must also consider any applicable regulatory requirements and must remember that the GIPS standards for FMPs are ethical standards based on the principles of fair representation and full disclosure. Any performance information presented must adhere to these principles.

All Fiduciary Management Providers are reminded that, above all else, they must follow all applicable laws and regulations regarding the calculation and presentation of performance, including all recordkeeping requirements.

Provision 31.A.20

The FIDUCIARY MANAGEMENT PROVIDER is responsible for its claim of compliance with the GIPS standards for FMPs and MUST ensure that the records and information provided by any third party on which the FIDUCIARY MANAGEMENT PROVIDER relies meet the REQUIREMENTS of the GIPS standards for FMPs.

Discussion

A Fiduciary Management Provider that claims compliance with the GIPS standards for FMPs is responsible for its claim of compliance. Therefore, a Fiduciary Management Provider that uses a third party to provide any service (e.g., custody or performance measurement), and relies on that service, must ensure that the records and information provided by the third-party service provider meet the requirements of the GIPS standards for FMPs. The Fiduciary Management Provider is responsible for ensuring that the data received from various external sources is accurate and must be able to aggregate information that may be supplied by external service providers as needed. A Fiduciary Management Provider should carefully research any third-party service provider and should engage only reputable service providers.

It is acknowledged that, in some cases, it may be challenging to obtain information from a third party that meets the requirements of the GIPS standards for FMPs. A Fiduciary Management Provider has the option of bringing performance in house rather than placing reliance on a third party. A Fiduciary Management Provider can also make adjustments to the information provided by a third party so that it meets the requirements of the GIPS standards for FMPs. For example, if a Fiduciary Management Provider received from a third party an asset-weighted composite return, the Fiduciary Management Provider could recalculate the composite return by equal-weighting the scheme relative returns to ensure compliance. As another example, suppose that a custodian reflects interest income on a cash basis. The Fiduciary Management Provider may make adjustments to the income information from the custodian to properly reflect accrued income.

When using third-party service providers, Fiduciary Management Providers are encouraged to ensure that adequate service-level agreements are in place to provide the historical records necessary, both currently and as needed in the future. It may be helpful to partner with custodians, administrators, prime brokers, and investment managers that understand what is needed to comply with the GIPS standards for FMPs.

Fiduciary Management Providers must establish policies and procedures to ensure that third-party information provided by a custodian or an underlying external manager adheres to the requirements of the GIPS standards for FMPs, if the Fiduciary Management Provider places reliance on that information. A thorough examination of third-party service providers’ policies and procedures should be conducted when they are hired. It is recommended that Fiduciary Management Providers who claim compliance with the GIPS standards for FMPs conduct periodic testing or other monitoring procedures that ensure that the policies and procedures of any third-party service provider on which the Fiduciary Management Provider relies have not changed since the service provider was first hired and are being applied consistently and appropriately.

Provision 31.A.21

The FIDUCIARY MANAGEMENT PROVIDER MUST NOT include THEORETICAL PERFORMANCE in the GIPS COMPOSITE REPORT.

Discussion

Because the intent of the GIPS standards for FMPs is to accurately and fairly represent actual Fiduciary Management Provider performance, no theoretical performance is permitted in the GIPS Composite Report. Theoretical performance is performance that is not derived from a scheme or composite with actual assets invested in the strategy presented. Theoretical performance comes in many forms including model, backtested, hypothetical, simulated, indicative, and forward-looking performance.

Provision 31.A.22

Changes in the FIDUCIARY MANAGEMENT PROVIDER’s organization MUST NOT lead to alteration of historical performance.

Discussion

Over time, the organization of a Fiduciary Management Provider may change. For example, a Fiduciary Management Provider may transition from a private to a public corporation, or a management buyout may result in a publicly traded company becoming a private entity. Regardless of the reason for the change in a Fiduciary Management Provider’s organization, historical composite performance must remain part of the Fiduciary Management Provider’s history. In considering issues regarding the use of historical performance, it is important to remember that performance is the record of the Fiduciary Management Provider, not of the individual. For example, suppose that a sole investment decision maker for a composite leaves a Fiduciary Management Provider and the new portfolio manager continues to manage the composite according to the same investment mandate or strategy as the previous manager. The Fiduciary Management Provider must link the historical performance of the composite to the ongoing performance achieved by the new manager.

Provision 31.A.23

The FIDUCIARY MANAGEMENT PROVIDER MUST present only performance that is in compliance with the GIPS standards for FMPs in GIPS COMPOSITE REPORTS.

Discussion

The GIPS Composite Report may include only performance that is compliant with the GIPS standards for FMPs. This requirement ensures that the information presented in a GIPS Composite Report is comparable between Fiduciary Management Providers. Non-compliant performance may not be presented. Non-compliant performance includes, but is not limited to, the following:

- asset-weighted composite returns,

- non-portable composite returns, and

- theoretical performance (e.g., hypothetical, model, and backtested performance).

Provision 31.A.24

Performance from a past FIDUCIARY MANAGEMENT PROVIDER may be used to represent the historical performance of the new or acquiring FIDUCIARY MANAGEMENT PROVIDER and LINKED to the performance of the new or acquiring FIDUCIARY MANAGEMENT PROVIDER if the new or acquiring FIDUCIARY MANAGEMENT PROVIDER meets the following REQUIREMENTS on a COMPOSITE-specific basis:

- Substantially all of the investment decision makers MUST be employed by the new or acquiring FIDUCIARY MANAGEMENT PROVIDER (e.g., research department staff, portfolio managers, and other relevant staff);

- The decision-making process must remain substantially intact and independent within the new or acquiring FIDUCIARY MANAGEMENT PROVIDER;

- The new or acquiring FIDUCIARY MANAGEMENT PROVIDER MUST have records to support the performance; and

- There must be no break in the track record between the past FIDUCIARY MANAGEMENT PROVIDER and the new or acquiring FIDUCIARY MANAGEMENT PROVIDER.

If any of the above REQUIREMENTS are not met, the performance from a past FIDUCIARY MANAGEMENT PROVIDER MUST NOT be LINKED to the ongoing performance record of the new or acquiring FIDUCIARY MANAGEMENT PROVIDER.

Discussion

When all or some investment management staff from a Fiduciary Management Provider join a new Fiduciary Management Provider, the performance of a past Fiduciary Management Provider may be linked to or used to represent the historical performance of a new or acquiring Fiduciary Management Provider if all of the following requirements are met on a composite-specific basis:

- Substantially all of the investment decision makers (e.g., research department staff, scheme managers, and other relevant staff), are employed by the new or acquiring Fiduciary Management Provider;

- The decision-making process remains substantially intact and independent within the new or acquiring Fiduciary Management Provider;

- The new or acquiring Fiduciary Management Provider has records that document and support the performance; and

- There is no break in the track record between the past Fiduciary Management Provider and the new or acquiring Fiduciary Management Provider.

If all of these portability requirements are met, the historical track record for the composite from the past or acquired Fiduciary Management Provider may be ported and linked to the continuing composite track record at the new or acquiring Fiduciary Management Provider and presented as a continuous track record. Although linking the track record is not required, it is best practice to do so.

If the Fiduciary Management Provider does not meet all of these portability requirements, it may not link the track record from the past or acquired Fiduciary Management Provider. The actions that a Fiduciary Management Provider may take with respect to the use of the composite track record from the past Fiduciary Management Provider will depend on which require-ment(s) cannot be met. In all cases, performance from a past Fiduciary Management Provider must never be presented when the new or acquiring Fiduciary Management Provider does not have records to document and support the performance. Suppose that the new or acquiring Fiduciary Management Provider has records that document and support the performance from a past Fiduciary Management Provider, but one or more of the other portability requirements are not met. In such a case, performance from the past or acquired Fiduciary Management Provider must not be linked to performance at the new Fiduciary Management Provider. For guidance on situations in which a break occurs in the track record between the past Fiduciary Management Provider and the new or acquiring Fiduciary Management Provider but all other portability requirements are met, see Provision 31.A.25.

For a Fiduciary Management Provider to be able to link the track record from the past Fiduciary Management Provider to the ongoing composite performance at the new Fiduciary Management Provider in a GIPS Composite Report, the track record must include all schemes that were managed in the strategy at the past Fiduciary Management Provider – that is, it must be composite performance. Where the provision states “on a composite-specific basis,” the word “composite” refers to the entire composite from the past Fiduciary Management Provider, not a subset of schemes. This is true even if the past Fiduciary Management Provider did not claim compliance with the GIPS standards for FMPs. Although the GIPS standards for FMPs do not have a requirement that all schemes must transfer from the past Fiduciary Management Provider to the new Fiduciary Management Provider, the Fiduciary Management Provider must have all the records needed to document and support the entire composite performance history. If the new or acquiring Fiduciary Management Provider cannot create a complete composite track record from the past Fiduciary Management Provider and can only create the track record using a subset of schemes, that information cannot be linked to the track record of the composite at the new or acquiring Fiduciary Management Provider in a GIPS Composite Report.

Outside of a GIPS Composite Report, an acquiring Fiduciary Management Provider that has records for only a subset of schemes in a composite from a past Fiduciary Management Provider may link the performance of the subset of schemes in the composite to the ongoing performance of the composite at the new Fiduciary Management Provider if the linking is requested by a prospective client. The linked information may be presented in a one-on-one presentation that is created for and will be used only by the prospective client.

The linked information may also be presented outside of a GIPS Report if the following conditions are met:

- The linked information is presented in a one-on-one presentation that includes the delivery of a GIPS Composite Report, if the corresponding GIPS Composite Report has not been previously delivered to the prospective client;

- The linked information is presented only to prospective clients who the Fiduciary Management Provider believes are sufficiently knowledgeable about investments and can understand the relevance and limitations of the track record being presented;

- There are sufficient disclosures regarding the linked information so that prospective clients understand that this is not a GIPS-compliant track record. Disclosure, however, does not necessarily prevent information from being false or misleading;

- The linked information is not presented if a GIPS-compliant track record is requested; and

- The linked information is not included in a consultant database.

If an acquired Fiduciary Management Provider is compliant with the GIPS standards for FMPs, the performance history meets the portability requirements, and the new or acquiring Fiduciary Management Provider chooses to port the performance, then the Fiduciary Management Provider must port the entire compliant track record that was presented by the acquired Fiduciary Management Provider. If the ported track record is longer than 10 years, the acquiring Fiduciary Management Provider may choose to present only a 10-year track record in GIPS Composite Reports.

If a Fiduciary Management Provider wishes to port performance from an acquired non-compli-ant Fiduciary Management Provider and link it to the Fiduciary Management Provider’s ongoing performance, if it is possible, it must build a composite track record from the prior Fiduciary Management Provider of at least five years, or since inception if the composite has been in existence for less than five years. If it is not possible to build a composite track record from the prior Fiduciary Management Provider of at least five years, or since inception if the composite has been in existence for less than five years, it must build the history for as long as the Fiduciary Management Provider is able to do so.

There may be cases in which a similar strategy is managed by the past Fiduciary Management Provider and the new or acquiring Fiduciary Management Provider. The new or acquiring Fiduciary Management Provider cannot combine the pre-acquisition track records or assets of a composite from the acquired Fiduciary Management Provider with a composite from the acquiring Fiduciary Management Provider and then show the combined track record or assets as GIPS-compliant information. The Fiduciary Management Provider must determine if it will use the track record from the past Fiduciary Management Provider or use its own track record. On a prospective basis, the ongoing composite may consist of schemes from the past Fiduciary Management Provider that have transferred to the new or acquiring Fiduciary Management Provider and continue the same investment mandate or strategy as well as schemes from the new or acquiring Fiduciary Management Provider that meet the definition of the composite.

Example